Over the last year, I’ve written a number of articles about small businesses. One of the most frequently asked questions is, “What exactly is my firm worth?” Fortunately, I can tell you with absolute precision that the answer is… “it depends!” It depends on the profitability of your business, and it depends on how long you have been in operation. It depends on how your business fits into the buyer’s organization. And it depends on who you ask. I’ve seen multiple buyers offer under 1 times profit for a business while the seller is sure that they are worth at least 6 times.

I’ve seen both the buyer and seller on a deal paying to get a professional valuation, by valuation experts, and coming up with completely different numbers. Formulas are rarely the same, so we shouldn’t be surprised that sellers tend to choose a formula or a source of information that is usually high, and buyers usually choose a process that leads to a low number. That’s just human nature. So, today, we’re going to go past formulas and opinions and look at real data on businesses that are being sold today. Let’s jump right in and see what your small business is worth!

We need to understand a little bit about methodology and focus on service companies. Why? First, they are simpler to deal with. A supermarket, farm or factory has equipment, inventory, and land to deal with. Each of those assets has a different process for valuation. Land can be very difficult to value if there have been no land sales in the area for a long time. Inventory is usually sold at a significant discount (30% or more), rather than at the purchase price. Cars and trucks use blue book prices, but very specialized mechanical equipment in a factory is harder to price. The second reason for focusing on service companies is that 80% of all employees in the US work in the service sector.

Many 1st time sellers make a big mistake by trying to use data from publically traded firms as their basis for valuation. Publically traded firms are sold for much higher valuations than small businesses. Publically traded firms pay millions of dollars in fees to investment banks and consulting firms in order to be on stock exchanges. They follow very stringent standards, and must meet standards for revenue and other business performance standards. This ensures that they are considerably greater value than the average small business, and it is reflected in their higher value. Publically traded firms also provide much more information on their operations. The Security and Exchange Commission (SEC), the primary government regulator for publically traded firms in the U.S., requires annual and quarterly reports on all aspects of operations. Privately owned small businesses rarely reveal any information at all. Private businesses must put in a lot of effort to find firms to buy and sell, to say nothing of what to pay.

While small businesses cannot turn to public data for valuation, there are private websites that sell firms. The biggest and the best of these is BisBuySell.com. With over 45,000 active listings, BizBuySell.com is the largest website in America for small businesses “classifieds”. BBS is partially owned by the Wall Street Journal, which used to be the dominant print publication for small business classifieds. BBS and their competitors are the evolution of classified ads. They not only allow you to buy and sell businesses, they also provide statistics on listings and sales.

Every quarter BBS produces “Insight” reports, aggregated information on market trends. Additionally, at any time, you can use their search engine to look for other firms that are similar to yours. You can see location, income, profit, asking price and other information. While income and profit are real (on the word of the seller), the asking price is what the seller wants to receive. In reality, the selling price runs about 15% lower than the asking price. In Q4 of 2015, the average asking price (for all businesses) was $230,000 and the selling price was $200,000. It’s difficult to say how many firms are sold, since a listing can be stopped and restarted under a new ID, an unsold firm may move to a different listing service, the owner may remove their listing and try again next year, etc. Over a full year period, only 16% of BBS listings are eventually sold.

Why are so few businesses sold? Classic economics tells us that if you aren’t selling enough of a product, the price is too high. However, I think it is more likely that the issue is visibility. It really is that hard for the right buyer and seller to find each other. Buyers don’t want it known that they are buying because it could raise prices. Sellers are even more cautious. The rumor or a sale can cause both customers and employees alike to flee. Once everyone knows that a sale will take place, it’s a matter of sell or die! At least, that’s what many small business owners believe.

There is some truth to this. The smaller the business, the more likely that the owner is a “one man show”. They run the business, take care of customer support and manage the clients. If they leave, there isn’t much left to sell. Larger firms generally have to delegate responsibilities, which provides some protection during a sale. The secrecy behind the sale of a small business makes it difficult for buyers and sellers to find each other. Unfortunately, that means that for all too many small businesses, the exit plan is to close their doors.

Now, let’s tighten our focus ever more, and just look at a specific type of service company, staffing firms. If you’re not a staffing firm, you probably think… “That’s pretty specific!” If you are a staffing firm, you’re thinking… “That’s not enough information! Where are they located? What is their discipline? Tech should be more valuable than admin! And if they are SAP or other sub-disciplines, that should be worth even more!” The more we know about our own business, the more data we want!

Unfortunately, it is unlikely that you will be able to find that level of information. While the BBS database has 45,000 active listings, when I filtered for staffing firms and filtered for listings that showed Gross Income, Cash Flow (or EBITDA), Asking Price and, at least, $750,000 in income (below this it is a “home based business”), I only get 20 businesses. The same is true in any other detailed search. Yet, even from this small and unscientific sample, there are trends.

The key numbers for most businesses are the “multiples”. This is the multiplier that you apply to either your gross income or to EBITDA. Generally, the EBITDA multiplier is more reliable and of greater importance. A buyer is better able to understand what they will pay for a firm that generates a profit of $500,000 (without knowing the revenues) than it is to make a bid for a $10 million firm (when you don’t if there is any profit). Cash Flow is not the same as EBITDA and may not be the same as profit, but they are close enough to be used interchangeably. The multiple for Cash Flow, for our sample, is either 2.2 or 2.3 depending if you use a weighted or unweighted average. Let’s split the difference and call it 2.25. That means that a business with a profit of $100,000 has a value of $225,000. This just creates a baseline, and then all sorts of adjustments will be made to come up with a final number. However, please remember that this is based on the Asking Price, not the price that was paid. We know from earlier numb that the price paid is 15% less than asking, yielding a multiple of 1.9.

Some of you may be thinking, “Is that it?” or “ I can’t retire on that!” If you are a small business that earns a million dollars or so with a profit of around $100,000… it may not make sense to sell your business. Not as a retirement strategy. You might get a one-time payout that adds retirement portfolio, but it can’t serve as your entire retirement strategy. Non-service businesses might have property, inventory, and equipment that is worth far more than the annual revenue. However, these numbers are only averages. As your business gets older and grows larger, these mature firms tend to have a higher value. While not all older firms become bigger firms, few big firms are new. Being “established” does impact the value of your firm. Our sample size is too small be definitive, but let’s see what our sample looks like when we plot it.

Non-service businesses might have property, inventory, and equipment that is worth far more than the annual revenue. However, these numbers are only averages. As your business gets older and grows larger, these mature firms tend to have a higher value. While not all older firms become bigger firms, few big firms are new. Being “established” does impact the value of your firm. Our sample size is too small be definitive, but let’s see what our sample looks like when we plot it.

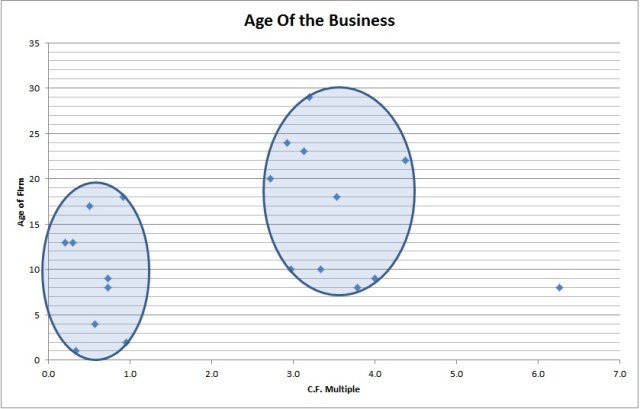

This chart plots all of the small businesses, showing the cash flow multiple against the age of the firm. I then put three bubbles on the chart, with each bubble being 1 multiple wide. As you can see, the first bubble takes in all but one outlier. However, the outlier is so close to the first bubble that we should include it in the same grouping (multiples of 1 or less). All firms under 5 years old are in this bubble, even though one firm is 17 years old.

Next we have an empty area between the 1st and 2nd bubble. No firms are selling for 1.5, 2, or 2.5 times cash flow. The 2nd bubble clearly contains older firms. The youngest are 10 years old, and the oldest is 29 years old. These firms have asking multiples of 2.5 to 3.5. The third bubble, which only has 3 firms, should contain the oldest firms, but this is not the case. Instead, firms in the 3rd bubble are younger than the previous bubble, but still older than the 1st bubble. If we join the 2nd and 3rd bubbles, we have the 1st group with low valuations, followed by a “dead zone” at 2-3 x cash flow and then the 2nd bubble with firms asking for a multiple of 2.7 and 4.4.

Let’s sum it all up! A lot of business are put up for sale every year, but not every business gets sold. Today, most businesses that are for sale are service businesses. Because service firms usually have no property, equipment or assets, the valuation process is simpler but valuation is never that simple. With many methods to calculate a valuation, no two individuals will produce the same numbers. To get a better idea of what is real, we extracted come live examples from the BizBuySell database. Overall, small businesses sell for around 3 times cash flow.

For our specific sample (staffing firms) we found that firms sold for multiples between 0.2 and 6.3. Obviously, anyone who wants to sell their business would far prefer to get a valuation of more than 6 rather than less than one. How do we get the higher valuation? There’s no single answer, but the most important factor seems to be the age of the firm, probably because older firms are on average larger and more profitable.

Overall, small businesses sell for around 3 times cash flow. For our specific sample (staffing firms) we found that firms sold for multiples between 0.2 and 6.3. Obviously, anyone who wants to sell their business would far prefer to get a valuation of more than 6 rather than less than one. How do we get the higher valuation? There’s no single answer, but the most important factor seems to be the age of the firm, probably because older firms are on average larger and more profitable.

That’s about it! You now have another tool and some guidance on how to value your firm. But in the end, the only thing that really matters is the deal that the buyer and the seller agree to. A valuation tells you something about what your firm is worth, but how you present your firm and how you negotiate will also impact the sale price. Whether you are the buyer or the seller, you need to listen to the other side, understand how they arrived at their price and always ask about the details. At least, that’s my Niccolls worth for today! If you’re buying or selling your business, give me a call and I might be able to help you put together a deal that fits your needs!